The AGI Windfall Mirage:

Why the First Lab to AGI Won’t Capture the Tens of Trillions It’s Chasing

By Alvin Wang Graylin 6/1/2026

(This is a long read, but a deliberate one, as the topic warrants it. I promise it will bring clarity to some critical misunderstandings that have pushed the AI industry and government policies in a dangerous direction. If it changes how you think about the AI industry, please pass it to someone who should see it too.)

A Mirage in the Mojave

Last summer, I was driving my family across the Mojave Desert. Somewhere west of Baker, California, the asphalt ahead of us began to shimmer. A wide silver lake stretched across the road, palm trees waving on its far shore. My daughter pressed her face against the window. “Dad, slow down. There’s water.”

I did not slow down. I kept driving. The lake retreated as we approached, then dissolved into hot air and salt flats. A few minutes later, it reappeared a mile further on. Then again. And again. Each time, my daughter insisted it was real. Each time, the desert insisted otherwise.

What she was seeing is called an inferior mirage. Hot air near the ground bends light, and your eyes, evolved to expect refraction only through water, draw the only conclusion they know how to draw. The brain is not lying. The physics is not lying. The interpretation is just wrong.

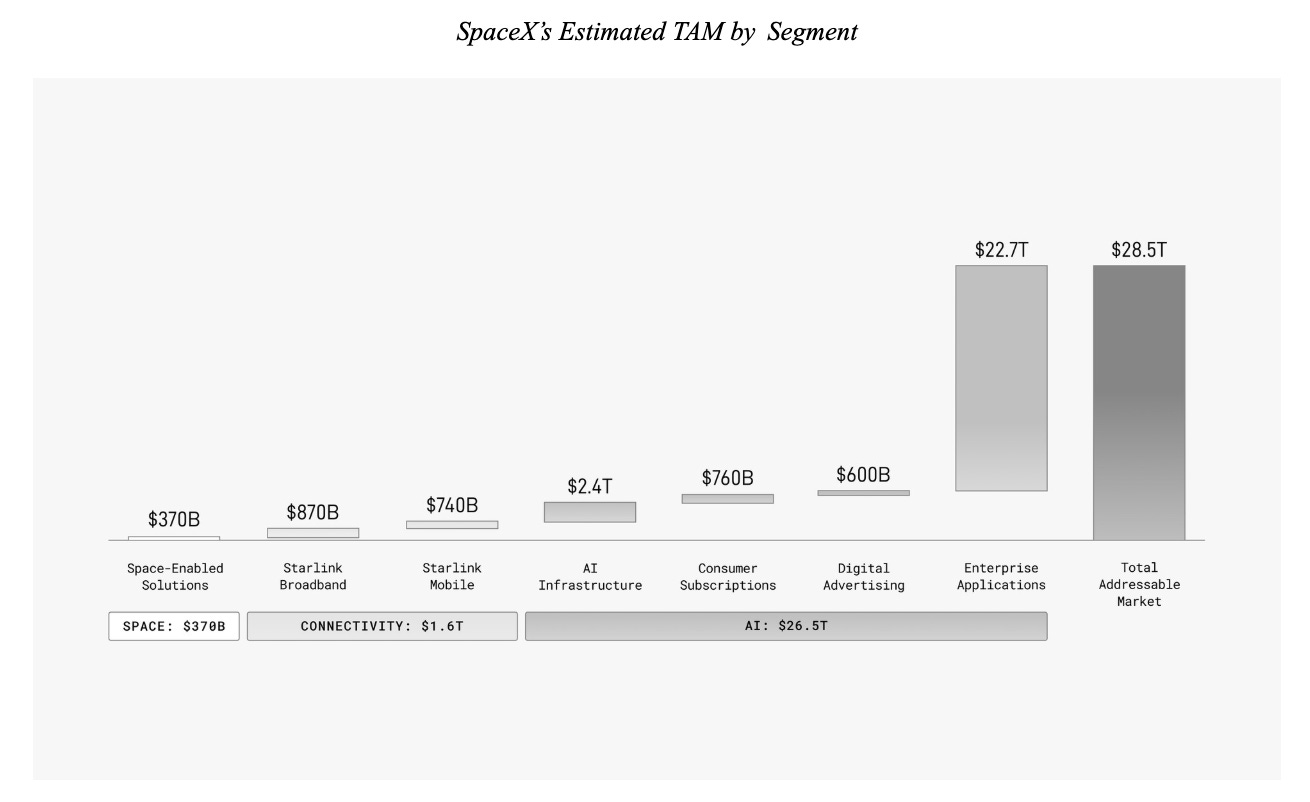

I have been thinking about that drive for the last year. Because the most powerful people in technology, finance, and government have stared into the heat shimmer of artificial general intelligence and reached the same confident conclusion my daughter reached. There is a lake out there. If we sprint hard enough, we will reach it first, and whoever reaches it first will drink uncontested for a century. There’s a common misperception among many AI lab heads and their investors that the first lab to achieve AGI will capture a windfall that approximately equates to the whole value of the white-collar labor market (annually ~$9 trillion in the US and ~$30 trillion globally). Most of them just talk about it privately to their friends, but Elon Musk’s SpaceX is saying the quiet part out loud. The newly published SpaceX S1 filings (which includes xAI, the company’s AI division) exhibits this assumption overtly. The filing’s single biggest target revenue segment, at roughly 80% of its $28.5T TAM, is what it calls the ‘Enterprise Application’ market (see figure below). Since the global IT and software market is only $5-6 trillion, the rest must reflect the company’s expectations for yearly gains from white-collar wage replacement.

Thus, spending a few hundred billion dollars in the next few years for that long-term prize should be a “no-brainer”, right? Unfortunately, it’s not that simple.

I want to argue, in this essay, that the lake is not there. That the “windfall” the first lab to AGI will allegedly capture is a mirage produced by the heat of capex overspending, the refraction of inflated stock prices, and the bent light of arms-race rhetoric. The race itself is real. The danger of failure (and success) is real. The potential of the technology itself is staggering. But the prize at the end, first-mover monopoly on superintelligence, is an optical illusion. And the policies built on that illusion are quietly setting fire to the world this technology is supposed to save.

I write this as someone who has spent 35 years inside the AI, semiconductor, telecom and cybersecurity industries on both sides of the Pacific. I have built four venture-backed startups enabled by AI, invested in over 100 and held executive roles at some of the biggest tech firms in the world. I’ve designed CPUs with GPU-like capabilities 10 years before Nvidia released CUDA. I’ve driven the construction of multiple global data centers across Asia. I’ve commercialized AI-driven natural language mobile search serving tens of millions of users on multiple carriers 17 years before ChatGPT released. I drove cybersecurity solutions for two of the largest firms in the industry. I started studying neural networks and natural language processing in 1990 and now do research on the economics of AI and associated policies at Stanford and teach it at the University of Washington. I currently advise governments, multilateral bodies, and Fortune 100 leaders on AI policy and post-AGI transition. I am a beneficiary of the AI boom, not a bystander. That is precisely why I think the bystanders deserve to be told the truth.

Eight Things You Will Not Hear at the Next AI Summit

Before we walk into the desert together, here are the eight counterintuitive and uncomfortable truths this essay will discuss. If even half of them are right, the current race strategy is not just wrong. It is a wealth-destruction machine wearing the mask of a moonshot.

• Cisco was right about the internet and lost 86% of its market cap anyway.

Being correct about the technology is not the same as capturing the value. The AI labs may be right on the power of the technology, but they won’t be able to get the ROI they hoped for.• Chinese AI labs can profit at one-tenth US training costs even after open-sourcing the model. Commoditization is not a side-effect of their strategy. It is the strategy.

• Frontier AI models are supercars. The global economy runs on buses, cars, and mopeds. Cheap, good-enough intelligence will eat the market the frontier models were supposed to own.

• There’s a chance that the GDP doesn’t grow much nominally from AI productivity gains. Meanwhile, the quality of life of the average person improves dramatically, making consumers the real winners. This would not provide a return to those investing trillions in AI today.

• AI labs are racing each other into a Cantillon-effect cliff they themselves helped build. Every dollar of training capex inflates the inputs of their nearest competitor, making the cost of future revenues ever more expensive while revenues per token are rapidly falling.

• The much-touted Jevons Paradox has an end point. Even as prices get cheaper, long-term demand stabilizes for any resource, including AI. The massive infrastructure buildout will find it increasingly difficult to earn a sustainable return on its investment.

• China is not racing to AGI. It is racing to diffusion, which is the only race that pays. Their “AI Plus“ plan targets 70% adoption by 2027 and 90% by 2030, while the United States spends trillions winning this week’s benchmark.

• In recorded history, no government has withstood a sustained nonviolent challenge from 3.5% of its population. AI is on track to alienate far more than that. The K-shape economy is not just unfair. It is unstable and unsustainable.

Let me show you the data behind each of these and then propose what to do about it.

The K-Shaped Amplifier: Whose Boom Is This?

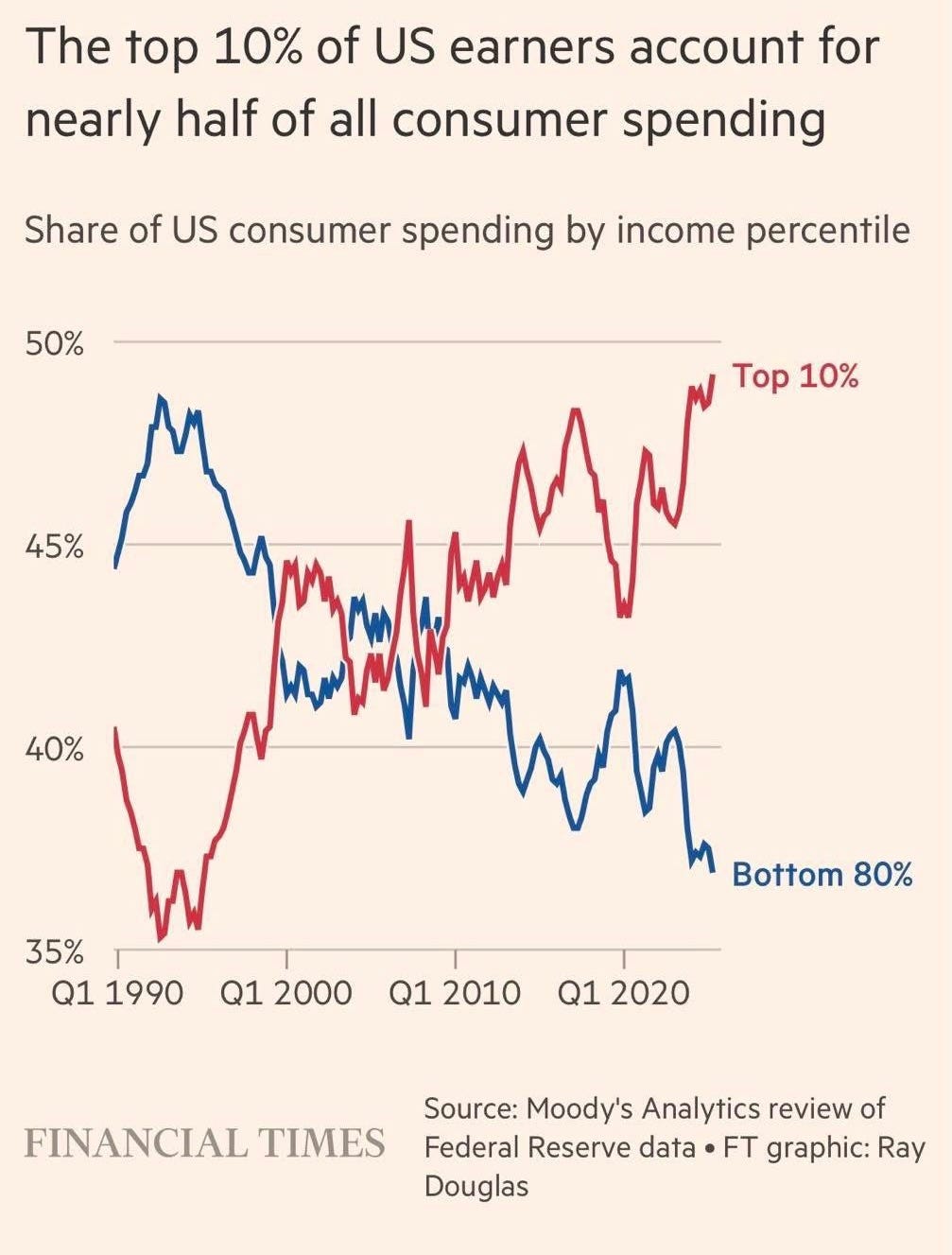

Start with the macro picture. Adam Tooze, writing in Foreign Policy on May 12, 2026, describes an American economy where “more than 49 percent of all consumer spending in the United States is now performed by the top 10 percent of U.S. earners.” (see figure below)

Innes McFee, CEO of Oxford Economics, told Fortune in January 2026: “Eventually, it might bring things together, but in the meantime…it’s unlikely that AI helps at all with the K-shaped economy.” Morgan Stanley’s Lisa Shalett has called the AI capex cycle “wackadoo” in scale relative to historical comparisons. Larry Fink at BlackRock has openly warned that the economy is bifurcating between asset owners and wage earners in ways that political systems have not historically survived.

This matters for our windfall analysis because it tells us where the money is actually going. It is not flowing to the workers whose tasks the models are eating. It is flowing to a thin band of equity holders, GPU suppliers, and infrastructure landlords (for now). And the AI labs themselves are not capturing it either. They are spending it! Even their internal forecasts are not expecting real profits for another 3-4 years. After finishing this piece, you may realize that may be overly optimistic.

Some readers will object that the K-shape is a temporary distortion, that displaced workers will find new jobs as every previous technology cycle eventually delivered. That is a fair objection, and it deserves a serious answer. The honest answer is that we do not know, but the structural evidence is worse than for previous transitions. In the past three industrial revolutions, it took 80, 60 and 40 years to play out, respectively, giving time for the economy and the population to adapt. This round of disruption could unfold in the next 5-10 years. Our society is not set up to accept such a shock.

The Stanford “Canaries in the Coal Mine” study finds that early-career workers in AI-exposed occupations are already losing positions. The World Bank estimates that over 60% of US jobs are AI-exposed, the highest share in the world, yet we don’t have any preparations for or a social safety net to protect the affected workforce. The transitional friction window is not a footnote. It is the policy problem.

The Cisco Lesson: Being Right and Losing Anyway

Here is the story that nobody at the labs wants you to internalize. In January 1999, Cisco was the company selling the picks and shovels of the internet revolution. Anyone who looked at the data could see the internet was not a fad. Cisco shares rose 236% in the next fourteen months. In March 2000, Cisco surpassed Microsoft to become the world’s most valuable company at a market capitalization of roughly $555 billion. Analysts predicted it would be the world’s first trillion-dollar firm.

Then the dot-com bubble burst. Cisco shares fell 86 to 88 percent over the next two years, wiping out approximately $431 billion in shareholder value. Cisco’s revenue kept growing. Its net income recovered. The internet kept eating the world, exactly as the bulls predicted. And yet Cisco stock did not regain its March 2000 peak until December 2025, more than a quarter century later.

Cisco was right about the internet. Cisco helped build the internet. Cisco still lost.

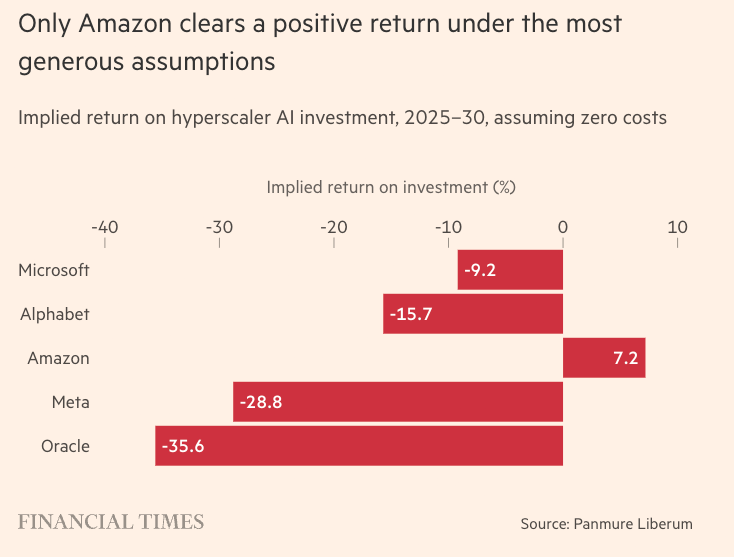

A common objection here is, “But Anthropic just hit $44 billion ARR in May 2026, up roughly 40x from a $1 billion run rate at the start of 2025. If AI is commoditizing, how is that possible?” It is a legitimate question and it deserves three clear caveats. First, much of that revenue is what I will charitably call a “token-maxing” frenzy driven by the rush to deploy agents, which is now getting a reality check. There is no moat and no loyalty. That rapid near term growth is primarily pushed by novelty plus inelastic enterprise demand for a tool with no nearby substitute. Both will compress. Second, the federal government’s February 2026 decision to blacklist Anthropic as a “supply chain risk” and shift defense workloads to OpenAI demonstrates how fragile concentrated enterprise revenue can be when politics intervenes. Additionally, Anthropic benefited from a rush of paid subscribers defecting from OpenAI in protest to them signing the Pentagon deal, fueling some near-term revenue growth in Q2. Third, the compute side is becoming visibly circular. Hyperscaler “other income“ from equity stakes in private AI companies accounted for nearly 60% of Alphabet and Amazon’s Q1 2026 income, money the hyperscalers invest in labs that then sign multi-gigawatt compute contracts back to the hyperscalers. xAI’s deal to backfill Anthropic capacity using SpaceX-aligned compute is the same pattern. The FT chart below shows the expected AI ROI for the major US hyperscalers assuming they have zero operating costs for the data centers. This should be troubling.

All the major US private frontier labs are preparing for their IPO as soon as possible, so everything being posted by them near term must be looked at with that lens in mind.

Cisco in 1999 also had no nearby substitute. Cisco’s revenue grew. The wipeout came not from the technology being wrong but from the valuations being divorced from the cash flows the technology could ever generate. We are in a similar place. The question is not whether AI will transform the economy. The question is whether the company that builds the smartest model captures the value or watches it leak past them like water through a sieve.

The Wage Bill Is Already Leaking

Where does the leak go? It goes to the deploying firms and, eventually, to consumers. This is not speculation. It is now measured. In April 2026, the Stanford Digital Economy Lab published The Enterprise AI Playbook: Lessons from 51 Successful Deployments, authored by Elisa Pereira, me, and Erik Brynjolfsson, based on extensive interviews with organizations from 8 countries representing over one million employees.

The headline finding, stated in the foreword: “Across 51 enterprise cases, we found stories of transformation measured in weeks and others measured in years. Same technology, same use cases, vastly different outcomes. The difference was never the AI model. It was always the organization.” Across our sample, 77% of the hardest implementation challenges were invisible and intangible costs of change management, data quality, and process redesign, not technical issues. The biggest productivity multiplier was the operating model: agentic deployments using escalation-based human oversight delivered a 71% median productivity gain, versus 30% for approval-gated models.

The economically critical implication is that the lab does not capture this 71%. The deployer of the technology does (for now). And as inference prices fall, more of the surplus flows downstream to the firm and ultimately to the consumer through lower prices. This is the J-curve Brynjolfsson et al have been documenting for a decade: a short-term productivity slump as organizations restructure, followed by a payoff that the people who built the technology rarely capture.

That same payoff structure produces a darker dynamic in the labor market. Brett Hemenway Falk and Gerry Tsoukalas modeled it formally in The AI Layoff Trap. Their result is bleak and important. Workers are also customers. When you fire them, they stop spending, which damages your competitors. In a competitive market, rational firms get trapped in an automation arms race that destroys consumer demand faster than the economy can rebuild it. As the authors put it, the result is “displacing workers well beyond what is collectively optimal.” When one firm automates, the laid-off workers’ lost spending damages every other firm in the market, but the automating firm bears only 1/N of the demand destruction. The trap is structural. Wage adjustments, capital income taxes, worker equity participation, UBI, and upskilling cannot eliminate it. “Only a Pigouvian automation tax can,” the authors conclude.

A Pigouvian tax, named for the British economist Arthur Pigou, is a levy designed to align private cost with full social cost by pricing in the externality that the market fails to capture. Carbon, petro and tobacco taxes are some familiar examples. For automation, the externality is the demand destruction that each displaced worker imposes on every other firm in the economy. Implementation options worth serious debate and piloting include a per-token surcharge on commercial AI inference (or robot tax), scaled to labor-displacement intensity, which would raise the marginal cost of substituting machine cognition for human work; a tiered tax on hyperscaler data-center construction and operation, set above the rates that apply to ordinary retail or commercial real estate, which captures rents from the physical instantiation of the labor-substituting capital stack; and a graduated automation-payroll levy on firms whose AI-driven labor reductions exceed a defined threshold. These taxes will effectively redistribute the expected value surplus the AI factories had planned to receive and likely slow down the deployments allowing more time for the economy to adapt.

This tax revenue will fund the social ballast, UBII and retraining, that the layoff-trap model identifies as necessary. The price signal itself has a second-order benefit the windfall narrative misses. Making frontier inference more expensive accelerates the migration toward smaller, distilled, and edge-deployable models, which is precisely the direction in which value capture democratizes, both inside high-income economies and globally, including in the markets where the next several billion users live and where today’s frontier API pricing would otherwise lock them out. The tax internalizes the externality and accelerates diffusion at the same time.

AI is genuinely capable of displacing 80%+ of workers’ tasks in multiple industries today and that impact will only grow as their capabilities expand over time, but most firms haven’t yet deployed properly to realize the potential. These are two facets of the same fact. A collection of tech firms have already accelerated AI related layoffs this year. The capability is real. The capture is broken. The lab gets the bill, the deployer eventually gets the surplus, and the laid-off worker subsidizes both by losing the job and the spending power.

The Coming Deflation and the Musk 10x Fallacy

Elon Musk has said publicly that AI will cause US GDP to grow 10x in a decade. I want to take this claim seriously enough to refute it.

For the GDP to grow 10x in ten years (~26% growth/year), prices would have to either inflate enormously or stay constant while real volume increased tenfold. Inflate by an order of magnitude and you destroy the monetary system. Hold constant and you contradict the mechanism that makes AI valuable. If a loaf of bread costs $4 today and AI lets bakeries make ten times as much bread, the bread does not stay at $4. The bread falls toward $0.40, because that is what competition does. Bakery revenue per loaf collapses. Bakery profits do not necessarily fall, because input costs (wheat, energy, labor) fall too, but the dollar GDP contribution of bread collapses even though caloric production rises tenfold.

This is the Acemoglu point, expressed as a price story. In The Simple Macroeconomics of AI, Daron Acemoglu walks through the task-by-task math and concludes that AI will deliver “no more than a 0.66% increase in total factor productivity (TFP) over 10 years,” with the most-likely figure below 0.53%. A common critique is that Acemoglu is the bearish outlier and underestimates the technology. This may be true, but he’s not alone. Goldman Sachs’s Joseph Briggs and Devesh Kodnani put the baseline AI productivity boost at around 1.5% over a decade. The most aggressive published estimate I am aware of remains roughly 3%. None of these will 10x GDP. None of these is even one extra full percentage point of trend growth per year.

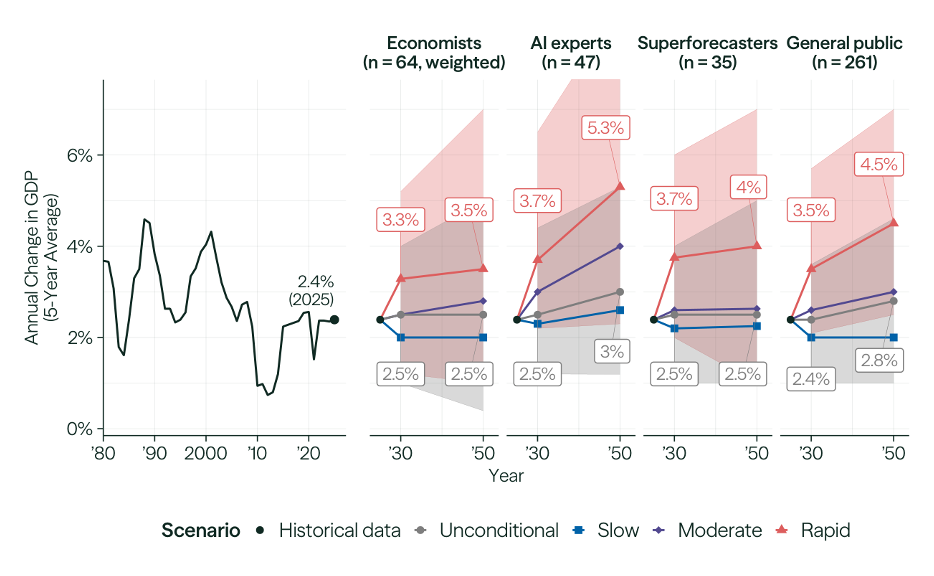

A more recent and broader survey makes the point even sharper. The NBER’s April 2026 working paper Forecasting the Economic Effects of AI by Karger et al elicited GDP growth forecasts from five distinct groups: academic economists, AI industry professionals at frontier labs, AI policy researchers, superforecasters, and the general public. The median respondent in every group, including the researchers and engineers working inside the AI companies themselves, projected annual US GDP growth of roughly 2.5% through 2030. That sits modestly above the typical Congressional Budget Office (CBO) long-run baseline of 1.7%, but it is two orders of magnitude below the 10x story. Even conditional on a “rapid” scenario in which AI surpasses humans across most cognitive and physical tasks by 2030, the AI-expert median for 2025 to 2050 annual GDP growth tops out at 5.3%, the economists’ median at 3.5%, the superforecasters’ at 4.0% (see figure below). None of these is 10x. None of these even doubles trend growth. And across all groups, the rapid scenario is judged less probable than either the slow or moderate path.

The gap that matters is not between the bulls and the bears. It is between the people building these systems and the people raising capital on them. The same firms whose CEOs publicly project transformative wealth creation employ technical staff whose own median forecast for the broader economy is roughly the CBO baseline. Either the staff are wrong, or the executive narrative is calibrated to a different audience: late-stage private valuations, prospective IPO roadshows, and federal compute commitments that require a story the internal forecasts do not tell.

What rising AI productivity actually produces, if competition is preserved, is mass deflation. The proper metric is not GDP. It is welfare. Brynjolfsson, et al developed exactly this metric in their GDP-B framework, published in the American Economic Journal: Macroeconomics. Their finding is striking: “improvements in smartphones cameras add approximately 0.63 percentage points per year” to welfare growth that does not show up in GDP. One product category. One narrow improvement. Nearly two-thirds of one percent of annual welfare invisible to the national accounts.

We get what we measure. Status hierarchies, capital allocation, and political legitimacy follow the metrics we publish. If we measure dollar GDP in a deflationary technology cycle, we will see decline where there is abundance. If we measure GDP-B, or the OECD Better Life Index, or Bhutan’s Gross National Happiness, we may finally see the actual ledger of what AI is delivering. A common rebuttal to mass deflation is “look at 1930s America or 1990s Japan, deflation kills demand.” Those were demand-collapse deflations from monetary contraction. A productivity deflation, where the same dollar buys ten times more bread, is a different animal. The policy challenge is not to prevent the falling price. It is to keep the laid-off baker fed while the bread becomes nearly free.

GDP Growth Paradox and Baumol’s Cost Disease

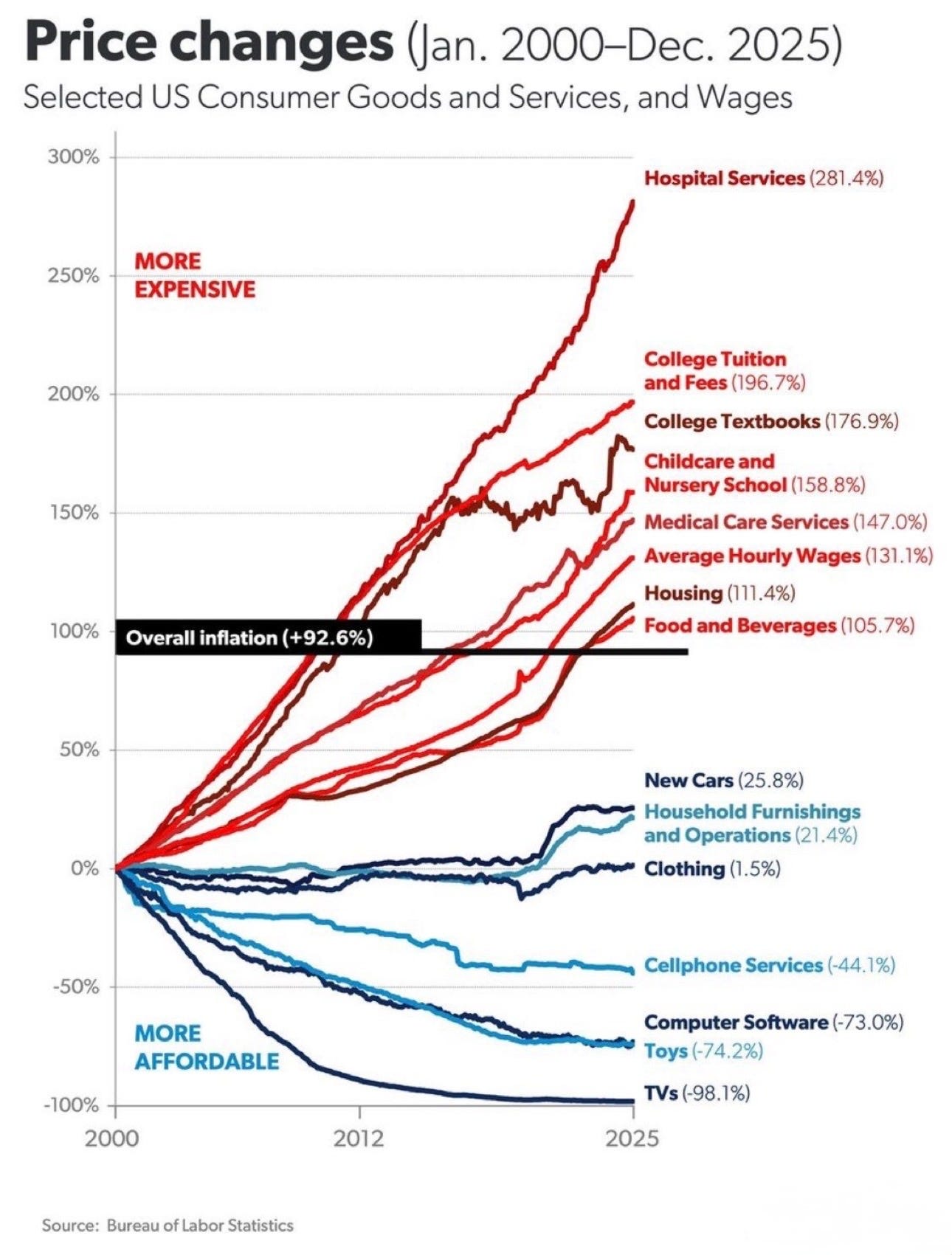

One counter intuitive consequence of the expected effective productivity gains from AI and robotics is that the total GDP may decrease. The GDP may actually shrink in nominal terms but grow faster than in the past on a purchasing power parity (PPP) basis due to deflationary effects. The figure below demonstrates the deflationary effects on prices of goods where production can be more readily automated. The reason some sectors increase significantly in price over time is mostly due to Baumol’s Cost Disease, where some services just can’t be automated even with improvement in technology. For example, a string quartet took 40 minutes with four musicians in 1800 and still takes 40 minutes to perform today. This constraint applies to many areas such as nursing, childcare, food services and education. The good news is that as more people are displaced in automatable sectors, there will exist a larger labor supply that can be redirected to take on more of the roles in the service sector thereby increasing affordability even in non-automatable sectors. The chart below from BLS shows areas where deflationary effects happening in recent years.

Economists generally are fearful of deflationary economies. This dynamic hinges on the difference between supply-side deflation (which is broadly beneficial) and demand-side deflation (which causes depressions). The divergence of Price and Quantity at its simplest, macroeconomic output is defined by a basic equation:

Nominal GDP = Price Level (P) x Real Output (Q)

Artificial intelligence, particularly as it reaches the level of highly capable, open-weight systems, acts as an unprecedented supply shock. It drives the marginal cost of cognitive labor, coding, legal analysis, and logistical planning toward zero. The Deflationary Vector (P) plummets: As the cost of intelligence collapses, the cost to produce almost everything else drops. This is a massive deflationary force, especially for cognitive services. The Productivity Vector (Q) skyrockets: Simultaneously, AI allows for a massive expansion in the volume and quality of goods, services, and software produced. If the percentage drop in prices (P) is greater than the percentage increase in output volume (Q), the total mathematical product (Nominal GDP) would shrink. However, because Q is expanding rapidly, the actual abundance of goods and services in the economy would be growing.

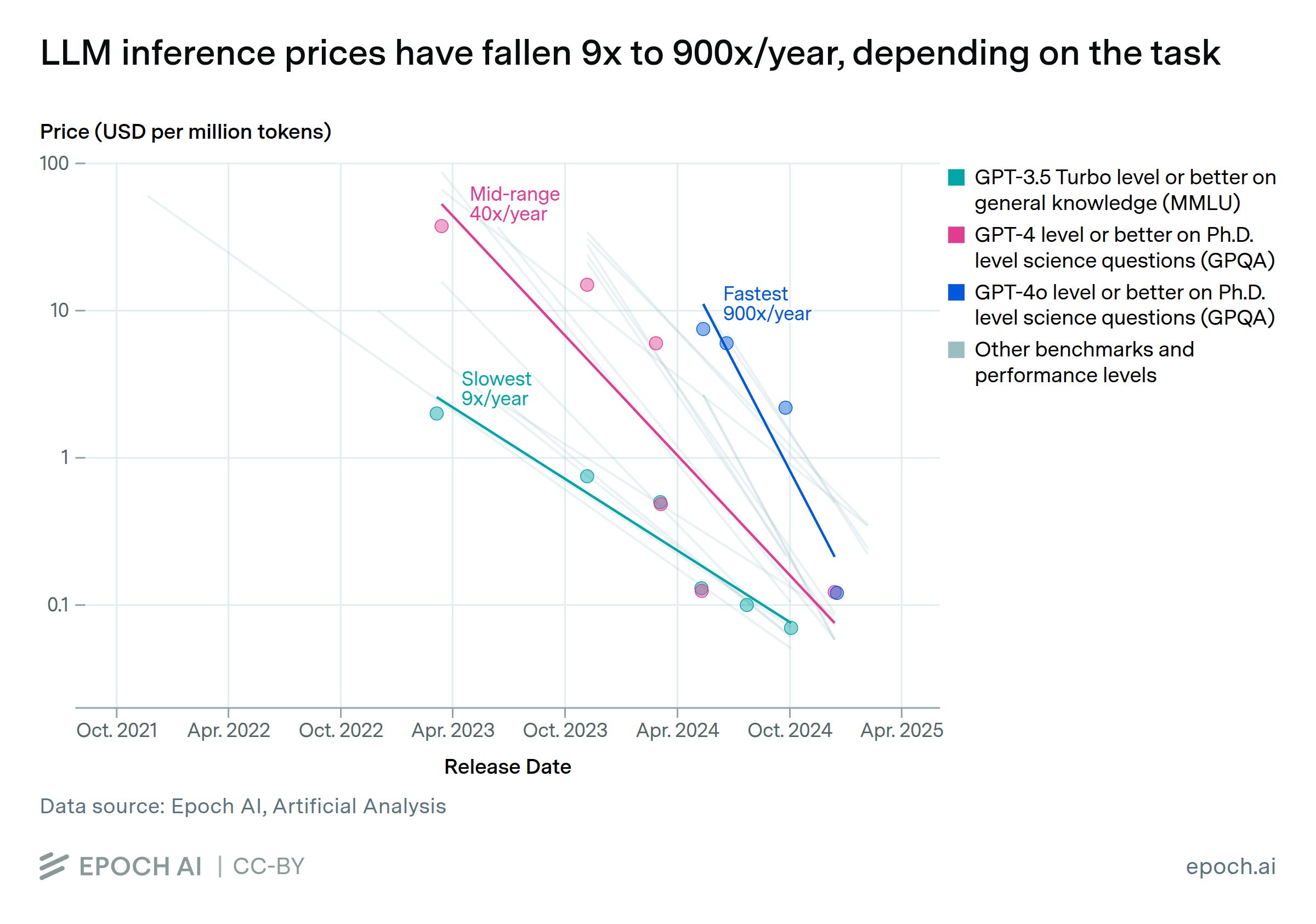

In real terms (adjusting for those massive price drops), purchasing power soars. A single dollar simply buys exponentially more computational power, healthcare diagnostics, and automated services than it did before. We already see this trend clearly: the price per token at the same quality of models is falling by over an order of magnitude per year (see figure below). Over time, as demand stabilizes, as it must, the efficiency gains could continue to improve and reduce nominal GDP as suggested above.

While the scale of AI is novel, the economic mechanism is not. Economists analyzing the “New Economy” have long studied how general-purpose technologies disrupt traditional output metrics by drastically lowering costs while boosting productivity (Nordhaus, 2002). During the late 19th century in the U.S., the combination of the telegraph, railroads, and electrification led to a sustained period of deflation. Prices fell continuously for decades, yet it was one of the fastest periods of real economic growth and rising living standards in American history.

The Debt Inflation Trap

The software-ization of the economy which has happened in the U.S. makes this possibility even more viable. Unlike physical manufacturing, AI services can be scaled infinitely at near-zero marginal cost. As a larger share of the economy moves from scarce physical goods to abundant digital or automated services, the total aggregate price level faces immense downward pressure. Recent macroeconomic models analyzing rapid AI adoption note that AI agents compress intermediary margins toward the cost of pure logistics. As AI becomes more capable, this could trigger a massive repricing across cognitive labor dominant sectors like SaaS, consulting, legal services, financial advisory, and insurance, etc., wiping out trillions of dollars in nominal economic “friction” while delivering similar utility to the end consumer.

While the math suggests my premise is possible, the reality of the political economy introduces severe friction. Shrinking U.S. nominal GDP could prove difficult to sustain. The U.S. government currently carries about $39 trillion in national debt. Debt is a fixed nominal obligation; it does not adjust downward when prices fall. If U.S. Nominal GDP shrinks, the Debt-to-GDP ratio mathematically explodes, making it increasingly difficult to service the debt through tax revenues, especially when taxable income will drop as workforce displacement expands into the higher income white collar segment. The monetary policy response of the Federal Reserve will likely be to fight AI-driven deflation aggressively. If AI drives prices down rapidly, central banks will likely respond by expanding the money supply (lowering interest rates, engaging in quantitative easing, or exploring direct fiscal transfers) to force the nominal price level back up to their target.

In fact, there are some in monetary policy circles who were hoping that what the AI lab heads are forecasting is true, so they could grow their way out of the massive national debt problem we have. Given what is discussed above, that hope may become increasingly difficult to realize, especially since the AI-exposed portion of the US economy is one of the biggest in the world, making a deflationary economy more likely as AI adoption effectively deepens in more sectors.

China Is Running a Different Race

If you believe the windfall thesis, you believe the United States is in a tight, winner-take-all sprint with China to AGI. China itself disagrees. In August 2025, the State Council released implementation guidelines for the “AI Plus” Initiative. The targets are stated explicitly: 70% adoption of next-generation intelligent terminals and agents across six key sectors by 2027, 90% by 2030. The plan also includes employment-protection language. In a 2025 ruling that Beijing’s labor bureau subsequently published as a “model case,” a Chinese court ruled that replacing a worker with AI is not valid grounds for dismissal absent attempts at retraining or reassignment. The diffusion plan and the worker-protection plan are paired.

China had earlier launched, in October 2023, the Global AI Governance Initiative, which has since evolved into a Global AI Governance Action Plan released in July 2025. Beijing is competing for the global standards regime, not for a single AGI threshold.

The cost data matters here. DeepSeek’s V4 Pro, released April 2026, prices at $0.44 per million input tokens and $0.87 per million output tokens, with cache-hit pricing at $0.0037. That is over 34x (86x priority mode) cheaper than GPT-5.5’s output price of $30 per million ($75 priority mode), and close to 137x cheaper on cached input. Anthropic’s Claude Opus 4.8 lists at $25 ($50 fast mode) per million output tokens, roughly 28x more (56x fast mode). Most other Chinese models are priced in the same range and will put significant pricing and margin pressure on the western frontier labs.

The objection here is that all of these benchmarks will move and that frontier models will keep an edge. That is correct. It is also irrelevant. Think of it as Savile Row versus the iPhone. There will always be a market for the bespoke tailor. That market does not set the global garment trade. The global garment trade is set by good-enough mass production. Once Chinese open-source models are within a few percentage points of the frontier on common tasks, and inference pricing is less than 1/10th, the global diffusion race may soon be effectively decided. The 2026 Stanford AI Index Report measures the gap at just 2.7% for the two countries. The frontier models are more like supercars today. The global economy runs on buses, cars, and mopeds. If the U.S. wants to have a play in global diffusion, it needs to act quickly in encouraging its AI labs to release more affordable vehicles that meet user needs.

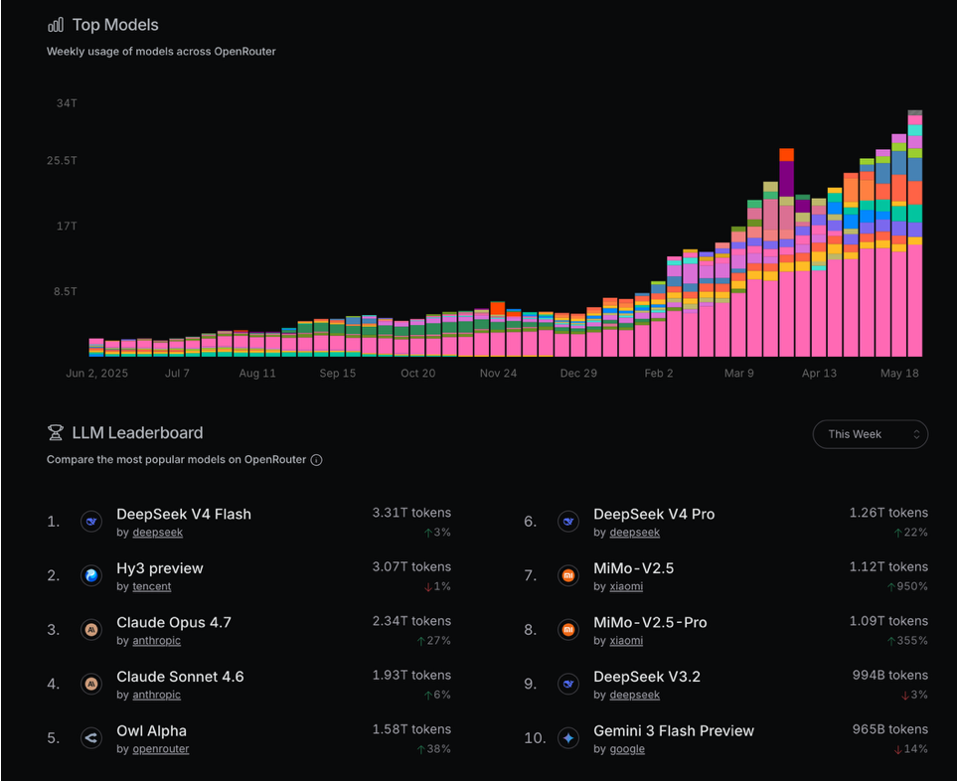

Per OpenRouter rankings (5/31/2026), six of the top 10 models used were Chinese open-source models. (see figure) In fact, it’s more accurate to say 7 out of top 10, as the Owl Alpha model from OpenRouter itself was fine-tuned on an anonymized Chinese open-source model. And this data doesn’t include the on-premise or edge deployments that many business customers deploy for open-source implementations due to privacy or regulatory constraints.

The second common objection: why would China keep open-sourcing models that the United States and others can copy? Because open-source is not generosity. It is industrial policy. Per Xinhua’s January 13, 2026 report confirmed by Hugging Face analytics, Alibaba’s Qwen family has crossed 700 million downloads on Hugging Face, “making it the most popular open-source AI system worldwide,” with the Qwen team confirming “more than 180,000 derivative versions” generated from its nearly 400 open-sourced models. Open-source drives cloud-service revenue, sovereign-AI partnerships across 150 Belt and Road partner countries, and a defensive moat against US compute denial. The same firm that profits at one-tenth US training cost can profit again on the cloud, on the inference, and on the diffusion. The strategy is internally consistent. The US strategy of model secrecy plus chip denial fights a war on terrain China has chosen not to occupy.

The Decisive Strategic Advantage Mirage

The deepest mistake fueled by the drive for the windfall is Silicon Valley advocacy for the Decisive Strategic Advantage (DSA) narrative. In my recent “Misdiagnosing the AI Race” essay for the Asia Society Policy Institute Center for China Analysis, I laid out why this dominant DC assumption being pushed by the AI and defense industries, that whichever country crosses the AGI threshold first locks in a permanent, globally dominant geopolitical position, is structurally unsound.

The DSA thesis depends on three claims, each falsifiable. First, that there is a clear finish line. There is not. AGI has many contested definitions, and AI development is a continuous, multi-dimensional process. Even if true, America’s nuclear monopoly, the closest historical analog, lasted only four years. Second, that capability gaps can be sustained through compute denial. Based on recent reports and AI benchmarks, the frontier gap with China has only narrowed over the last year, even with full denial in place, while multiple Chinese labs are training with and tuning for domestic Chinese GPU offerings. Third, that the dynamic is winner-take-all. In practice, Cursor leaderboard data from 2025 showed the top model changing nearly every month. There is no moat for AI models and no user loyalty.

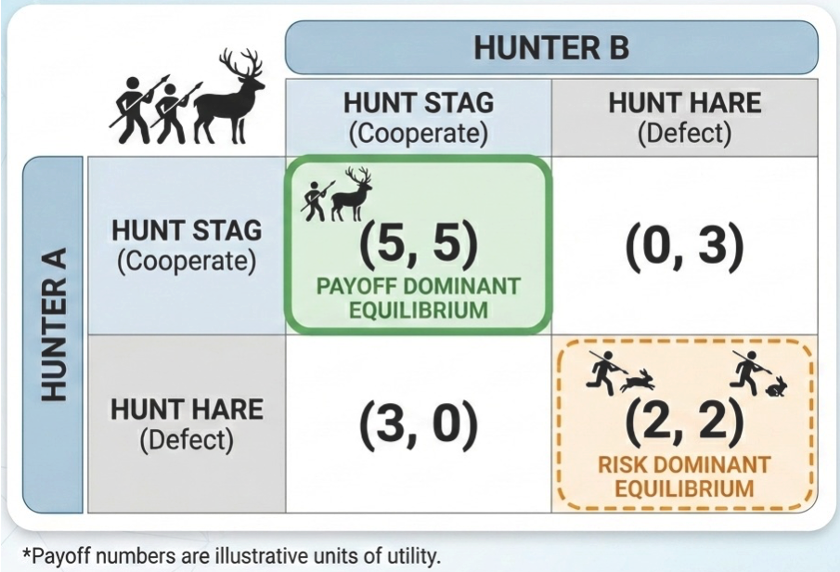

The deeper category error is treating the AI competition as an arms race (zero-sum, secretive, winner-takes-all) when what is actually unfolding is an innovation race and a platform race (positive-sum, ecosystem-driven, multi-winner). Even worse, US policy implicitly models the US-China dynamic as a Prisoner’s Dilemma when game theoretically it is closer to a Stag Hunt. In a Stag Hunt there are two Nash Equilibria, the two hunters can cooperate to catch the stag (safe and aligned AGI) or defect to hunt hares (good enough models that boost the economy). (See Payoff Table below) The worst possible outcome is precisely where the US finds itself today: attempting to hunt the stag alone (which is unlikely to be achieved alone) while the other player calmly collects hares. The more desirable strategy for the U.S. is to reduce capex investment near term to lessen economic strain until there’s more clarity on a clear path to a safe AGI implementation and begin some reasonable regulations on the AI labs, so their profit motives don’t create more harm than good. This helps reduce the shock of a massive market correction, gives more time for the economy to adapt to new market forces, and ensure greater safety from misuse or alignment issues. There may also be new algorithmic or architectural breakthroughs on the way that makes the current scaling focused approach unnecessary or obsolete.

This is not merely abstract. The US has committed over $800 billion in AI capex for 2026 while job openings have declined sharply since 2022. The military DSA argument is also weaker than advertised. Recent Iran operations were reportedly planned with Claude 3.5 Sonnet, a model already 20 months old at the time, because the Defense Department IL6 certification pipeline takes over 12 months. Whatever advantage a frontier US model confers, the institutional capacity to operationalize it is the binding constraint, and on that metric the US is structurally disadvantaged.

A reasonable counter is that defense and biosecurity warrant narrow carve-outs. They do. The right architecture is a “small yard, high fence” for genuine CBRNE (Chemical, Biological, Radiological, Nuclear, Explosive) and autonomous-weapons risk, paired with broad cooperation on diffusion, safety standards, and shared-risk monitoring. Today’s “small yard” has expanded to cover EDA software, HBM memory, chemicals, and frontier models. This kind of policy has only accelerated China’s push for technology independence and stifles the will for cooperation over shared risks from non-state bad actors when we need it most.

Jevons Paradox vs. Kuznets Curve

One last steelman to dispose of. The Jevons paradox argument goes: cheap inference will increase demand for inference enough that the labs win on volume. Maybe. But human attention is bounded, energy is bounded, and per-capita consumption in mature markets saturates. Jevons Paradox was based on cheaper energy in the form of coal driving more total demand for energy. What most people don’t talk about is that in the long run, energy use looks more like a Kuznets Curve. (Kuznets, coincidentally, invented the concept of GDP and long criticized its effectiveness at measuring true economic value.) The time series data of developed countries clearly shows that energy demand actually topped out as basic human needs are satiated. In western nations, that happened in the 1990s and even shows per-capita energy consumption declining despite electrification because efficiency outruns new demand in saturated economies. (see figure below) Humans have a point of satiation for all goods and services. The same logic will eventually apply to AI inference. Maybe even more so, as AI efficiency gains have been on the order of 40x per year the last few years. There is no infinite well of valuable tokens to produce and most users don’t need to run the latest high-performance frontier models to summarize documents or plan their travel. Eventually most consumer AI use cases will migrate processing directly to edge devices like PCs and phones both because of the efficiency improvements of the models but maybe more importantly due to the desire by most to protect their privacy.

When inference demand saturates and prices keep falling, the labs are caught between two walls: rising training costs (next-generation models cost more, not less, to train) and falling unit revenue (commodification of inference at a small fraction of the current premium prices). That is the Cisco trap. That is why the AGI windfall is a mirage. And racing to this mirage is exactly what’s making our economy more fragile and our world less safe.

The Soft Landing: Why 3.5% Matters?

Now we come to the part that keeps me up at night. The K-shape economy is not just an economic problem. It is a political one. And the political problem has a number attached to it.

In Why Civil Resistance Works, Erica Chenoweth and Maria Stephan compiled the Nonviolent and Violent Campaigns and Outcomes (NAVCO) dataset, studying 323 violent and nonviolent campaigns from 1900 to 2006. Their finding, formalized by Chenoweth in a 2013 TEDx talk and refined in her 2020 Carr Center discussion paper became known as the 3.5% rule. In her words: “no government has withstood a challenge of 3.5 percent of their population mobilized against it during a peak event.” Successful campaigns in the dataset include the Cedar Revolution, the Singing Revolution, the fall of communism in Albania, and the 2019 Sudanese revolution. As Chenoweth has noted in subsequent updates, authoritarian regimes have grown more adept at suppression since 2010, but the underlying mechanism, mass mobilization breaking elite cohesion, remains operative.

Three and a half percent of the US population is roughly 12 million people. AI’s projected labor exposure dwarfs that number by an order of magnitude.

The 3.5% rule does not stand alone. Walter Scheidel, in The Great Leveler shows that across recorded history only four forces have meaningfully compressed inequality: mass-mobilization warfare, transformative revolution, state collapse, and lethal pandemic. He calls them the Four Horsemen of Leveling. The implication should chill every CEO and policymaker reading this. The historical default is that high inequality persists peacefully until it does not, at which point it is reduced by catastrophe.

Peter Turchin’s End Times gives us the mechanism in real time. Turchin’s 2010 Nature forecast predicted that US political instability would peak around 2020, driven by “elite overproduction” and “popular immiseration.” The January 6, 2021, storming of the US Capitol, the polarization indices, and a decade of declining institutional trust have largely vindicated that forecast. Turchin’s Political Stress Index combines wage stagnation, elite competition, and state fiscal stress into a single indicator. AI’s labor displacement adds fuel to all three.

Daron Acemoglu and James Robinson, in Why Nations Fail drew the institutional version of the same lesson. Inclusive institutions, those that share broad-based prosperity, are stable. Extractive institutions are not. Political scientist Carles Boix, in Democracy and Redistribution, made the same point in plainer terms: democracies survive when ordinary voters believe their turn is coming. They fail when the lane that isn’t moving never starts moving. Albert Hirschman called this the “tunnel effect.” Stuck in traffic, you tolerate the wait so long as the next lane is also creeping forward. When only the express lane moves and yours sits still, patience snaps.

Stack these findings together. The AI K-shape hollows out institutions. The Layoff Trap deepens hardship at the bottom. Hyperscaler-lab capital recycling concentrates elite competition into a single sector. And history says that when even three and a half percent of a population mobilizes against this kind of configuration, regimes fall. We are building, with our own capex, a coalition of displaced workers, young graduates with no first rung on the ladder, and too many ambitious elites chasing too few elite positions. And we are doing it faster than any previous industrial transition.

History gives us proximate cases. The French Revolution followed an aristocratic capture of grain markets. The Russian Revolution followed wartime immiseration. The Iranian Revolution of 1979, the Eastern European cascades of 1989, the Arab Spring of 2011, the Sri Lanka uprising of 2022, all share the same anatomy. Cost-of-living grievance plus elite-mass perception gap plus a precipitating event. AI driven layoffs and non-hiring is the cost-of-living grievance. Trillion-dollar hyperscaler capex and accelerating billionaire wealth accumulation without broad gains is the perception gap. We are missing only the precipitating event. We should not wait to find out what it is.

What is the alternative? It is what I have called elsewhere Abundanism, and what the historical analogy of the Bonobo offers us.

The Bonobo Lesson and the Six Pillars

About two million years ago, the formation of the Congo River split a common ape ancestor into two populations. North of the river, scarcity. South of the river, fertile abundance. The same DNA. Different civilizations. North of the river, the chimpanzees developed alpha-male hierarchies, troop warfare, and dominance-based politics. South of the river, the bonobos developed matriarchal egalitarianism, sex as conflict resolution, and cooperative foraging. They are 99.6% genetically identical with each other but have developed cultures that are polar opposites. We share more than 98.5% of our DNA with both. We are not condemned to either. We have the advantage that we can adapt to the environment we choose to build.

For ten thousand years we built environments of scarcity. We designed economies, institutions, and conflicts around lack. The world the AI revolution makes possible is genuinely different. Marginal cost approaches zero for energy, computation, and increasingly matter. The bonobo configuration is, for the first time in recorded history, the economically rational configuration due to the technological progress we have collectively made as a species over thousands of years.

That is the foundation of Abundanism, the post-scarcity framework I introduced in Our Next Reality (Hachette, 2024) and have developed since on the Abundanist Substack. Abundanism rests on six pillars:

1 Governance with AI as Partner. AI as policy oracle and decision-support, not master, not servant. Where humans are biologically constrained, foresight, cross-domain synthesis, freedom from short-term emotional capture, AI can complement. An AI with deep understanding of perspectives from all countries and cultures will help us end conflict.

2 Post-Monetary Value Systems. Money will retain meaning during the transition and may even surge in value temporarily, then transition toward systems that price time, service, and social contribution. Redirecting benchmarks towards “GDP-B”-like metrics is an early waypoint on that road.

3 Universal Basic Income and Infrastructure (UBII). Not income alone. Income plus housing, healthcare, education, and connectivity as a floor. This becomes much more viable as cost of underlying goods and services deflate overtime due to the forces discuss above.

4 Purpose Engineering. When labor as a source of meaning is automated, we need new infrastructure for purpose, community, creativity and exploration. As a society, we need to celebrate service to others vs the number of commas in one’s bank account. Immersive technology, properly governed, can serve as a key part of that infrastructure to connect, enable and retrain the population.

5 Supply and Demand 2.0. Intelligent matching of human need to available capacity without prices as the sole mediating mechanism. When energy and intelligence move towards zero cost, the ability to produce what’s needs where it’s no longer needs price as a signal.

6 Education as Peace Technology. Universally personalized, AI-augmented education as the largest peace-dividend investment a society can make. A broadly and deeply educated population is core to long term human societal flourishing.

These pillars are how an Abundanist economy avoids the Layoff Trap. The Pigouvian automation tax Falk and Tsoukalas advocate becomes the funding mechanism for UBII. The diffusion advantage that China is building becomes the platform we should be racing them to expand and humanize. And the metrics we publish, GDP-B alongside GDP, OECD Better Life alongside payroll, Bhutan’s GNH alongside corporate earnings, become the dashboard against which we steer.

Beyond Rivalry and the Montreal Moment for AI

The geopolitical version of this same argument is what I developed in Beyond Rivalry: A US-China Policy Framework for the Age of Transformative AI in Stanford’s Digitalist Papers, Volume 2. The core proposal stack: a CERN for AI focused on joint global safety and innovation research; a Global Data Pool so that frontier models learn from globally representative data rather than the digital exhaust of two coasts; an IAEA for AI to regulate advanced AI for global good when it is achieved; a Guardian AI model that protects us from bad actors and ourselves; a Universal Basic Income and Infrastructure framework as the social ballast; a GI Bill for the AI Age to preserve displaced workers dignity and provide needed reskilling; and a Marshall Plan for AI to fund the post-AGI transition across the developing world. Not all these elements need to be established on day 1, but they can be rolled out as appropriate. We need to consider reframing the narrative from a winner-takes-all to a winners-share-all approach, otherwise there may be no winners at all.

There is a hard-headed self-interested case for treating advanced AI as a global public good rather than as an instrument of national or corporate dominance. Over the next decade, an estimated two to three billion people are projected to come online for the first time or upgrade to AI-capable devices, predominantly across South Asia, Sub-Saharan Africa, Southeast Asia, and Latin America. They are the next billion enterprise customers, the next billion knowledge workers, and the next billion consumers of intelligence-as-a-service. Labs and governments that help them arrive there, through low-cost models, locally grounded datasets, affordable inference infrastructure, and education-focused deployments, will capture more long-term enterprise and consumer value than any that try to dominate from above.

Global uplift also generates secondary returns that no income statement currently measures: social stability, reduced migration pressure, fewer brittle states, less motivation for extremist movements and the kind of broad-based real growth that historically correlates with reduced great-power conflict. The frame that the United States and China should treat advanced AI as a rivalrous national-security asset to be hoarded is the same frame that delivered Cisco-style value destruction in the original Internet build-out and that today produces the K-shape at home. The frame that treats advanced AI as a public good, governed multilaterally and deployed broadly, is the frame that pays.

The recent Trump-Xi Summit in Beijing opened a narrow door to exactly this kind of architecture. Treasury Secretary Scott Bessent told CNBC on May 14 that “the reason we are able to have wholesome discussions with the Chinese on AI is because we are in the lead.” That framing may be overstated, but the substantive opportunity is exactly right. President Trump confirmed the two governments are “considering establishing some kind of mechanism on guardrails,” echoed by Bessent’s reference to a “protocol on AI safety.” This is the closest we have come to a Montreal Protocol moment for AI.

A Montreal-for-AI is possible. The 1987 Montreal Protocol on ozone-depleting substances had universal ratification and led to the recovery of the ozone layer that is on track to be complete by mid-century. It worked because the threat was scientifically agreed, the substitutes were technologically available, and verification was tractable. AI safety can clear the first bar. AI labs can clear the second. Only governments, working together, can clear the third. The Asilomar conference of 1975 showed that recombinant DNA could be voluntarily paused by researchers themselves. The 2018 moratorium on heritable human genome editing, called in the wake of He Jiankui’s CRISPR babies, showed that even rivalrous nations can agree on a bright line. AI’s bright lines are not impossible to draw. They are politically inconvenient to honor.

Right now, no one is walking through the door the Trump-Xi summit cracked open. The strategic risk in front of us is not the invention of a single decisive model. It is the diffusion of many models we cannot recall, into the hands of bad actors we cannot deter, in a global economy where we have refused to talk to the other half of the technology stack.

Conclusion: The Oasis Is Real, but Not Where the Mirage Says

Back in the Mojave, my daughter finally accepted that the lake was not there. We pulled off at the Baker exit. She bought a Gatorade from a gas station and watched the desert through the window of an actual building, with actual air conditioning, and actual water. The oasis was real. It was just not where the heat shimmer told us to look.

The AGI Windfall Mirage is the same story. There is no single decisive lead. There is no permanent monopoly. There is no first-mover trillion-dollar prize that survives commoditization, deflation, geopolitical fragmentation, and democratic backlash. Anyone running toward that lake will arrive at a salt flat. The real oasis, the real win, is broader. It is multiple winners, each capturing a slice of an expanding pie, with the bottom 90% of the population not just included but structurally protected by UBII, retraining, AI-augmented governance, and global cooperation on safety.

I want to be crystal clear about the framing. The “Winners-Share-All” mentality mentioned earlier is not naivete. It is enlightened self-interest. Game-theoretically, the multi-turn Stag Hunt I described above pays better for the cooperators than for the defectors. Economically, the demand externality from mass layoffs destroys the consumer base that frontier AI labs depend on. The Layoff Trap is the producer’s nightmare, not the workers’. Politically, the 3.5% threshold is a fence around what elites can extract before regimes lose stability, and AI is on track to alienate an order of magnitude more than the needed threshold. Historically, the only forces that have ever leveled extreme inequality are catastrophic. We have one chance, in this decade, to choose a fifth horseman: voluntary, evidence-driven, broad-based redistribution coordinated across major powers before the other four ride.

To the AI labs and the VCs funding them: reevaluate your plan and your motivations. The current race is not worth running. It is constructing the conditions under which everyone loses. There is no glory in being first to a finish line that does not exist, especially if the cost of running there is the stability of the globe and sustainability of the financial system that would give your expected windfall actual value.

To the policymakers tasked with ensuring prosperity for your citizens: dig deeper, because you have been fed a fiction. The current race between the labs and nations will not deliver the economic growth or the broad wealth you have been promised. Whether AGI arrives in one year, five, or ten will make little difference to what we ultimately gain from it. But if the transition is managed poorly, it could trigger a disaster that takes decades to recover from. A rational approach, building and deploying this technology at a pace society can absorb, can bring real quality-of-life gains to everyone and unlock scientific breakthroughs on problems we have faced for centuries as a species. Treat safe AGI as a public good and find ways to share it with the world, not hoard it.

To the workers and citizens watching this from outside the labs: you are not powerless. The 3.5% rule cuts both ways. It can topple. It can also demand. Demand metrics that measure the abundance you actually receive. Demand institutional structures that put a Pigouvian floor under your displacement. Demand the GI Bill for the AI Age, the Global Data Pool, the CERN for AI. Demand the social infrastructure that preserves your dignity and enables global human flourishing. The technology and its benefits are real. The mirage is what we have been told to chase.

The short-term race to AGI is self-defeating and dangerous. The long-term race to broad-based abundance is the only race that pays. Let us run that one. Together.

“The builders of frontier AI cannot be trusted to resolve these magnificently complex philosophical questions alone, because they themselves operate within a system of incentives that can and probably in some instances does conflict with the good of humanity.”

- Christopher Olah (Anthropic Founder) at the Vatican

Endnotes

1 Adam Tooze and Cameron Abadi, “Tooze on the K-Shaped Economy and Its Global Effects,” Foreign Policy, May 12, 2026. https://foreignpolicy.com/2026/05/12/tooze-k-shaped-economy-us-ai-cantillon-wealth-distribution/

2 Innes McFee quoted in “Oxford Economics: AI is unlikely to help resolve K-shaped economy anytime soon,” Fortune, January 29, 2026. https://fortune.com/2026/01/29/k-shape-economy-reinforced-ai-wealth-effect/

3 “NVIDIA and the Cautionary Tale of Cisco Systems,” Harding Loevner. https://www.hardingloevner.com/insights/nvidia-and-the-cautionary-tale-of-cisco-systems/

4 “The Cautionary Tale of Cisco Systems,” Liberty Through Wealth, March 22, 2022. https://libertythroughwealth.com/2022/03/22/cautionary-tale-of-cisco-systems/

5 “Cisco’s stock closes at record for first time since dot-com peak in 2000,” CNBC, December 10, 2025. https://www.cnbc.com/2025/12/10/ciscos-stock-closes-at-record-for-first-time-since-dot-com-peak-2000.html

6 “Anthropic raises $30 billion in Series G funding at $380 billion post-money valuation,” Anthropic, February 12, 2026. https://www.anthropic.com/news/anthropic-raises-30-billion-series-g-funding-380-billion-post-money-valuation

7 “Anthropic says it hit a $30 billion revenue run rate after ‘crazy’ 80x growth,” VentureBeat. https://venturebeat.com/technology/anthropic-says-it-hit-a-30-billion-revenue-run-rate-after-crazy-80x-growth

8 “OpenAI announces Pentagon deal after Trump bans Anthropic,” NPR, February 27-28, 2026. https://www.npr.org/2026/02/27/nx-s1-5729118/trump-anthropic-pentagon-openai-ai-weapons-ban

9 Adam Tooze, “Chartbook 447: The US economy in May 2026,” May 2026. https://adamtooze.substack.com/p/chartbook-447-the-us-economy-in-may

10 Elisa Pereira, Alvin Wang Graylin, and Erik Brynjolfsson, The Enterprise AI Playbook: Lessons from 51 Successful Deployments, Stanford Digital Economy Lab, April 2026. https://digitaleconomy.stanford.edu/publication/enterprise-ai-playbook/

11 Brett Hemenway Falk and Gerry Tsoukalas, “The AI Layoff Trap,” arXiv:2603.20617, March 2, 2026. https://arxiv.org/abs/2603.20617

12 Tyna Eloundou, Sam Manning, Pamela Mishkin, and Daniel Rock, “GPTs are GPTs: An Early Look at the Labor Market Impact Potential of Large Language Models,” arXiv:2303.10130, August 22, 2023. https://arxiv.org/abs/2303.10130

13 Aditya Challapally, Chris Pease, Ramesh Raskar, and Pradyumna Chari, The GenAI Divide: State of AI in Business 2025, MIT Media Lab Project NANDA, July 2025.

14 Anton Korinek and Donghyun Suh, “Scenarios for the Transition to AGI,” NBER Working Paper 32255, March 2024. https://www.nber.org/papers/w32255

15 Daron Acemoglu, “The Simple Macroeconomics of AI,” NBER Working Paper 32487, May 2024. https://www.nber.org/papers/w32487

16 Ezra Karger, Otto Kuusela, Jason Abaluck, Kevin A. Bryan, Basil Halperin, Todd R. Jones, Connacher Murphy, Philip Trammell, Matt Reynolds, Dan Mayland, Ria Viswanathan, Ananaya Mittal, Rebecca Ceppas de Castro, Josh Rosenberg, and Philip Tetlock, “Forecasting the Economic Effects of AI,” NBER Working Paper 35046, April 2026. https://www.nber.org/papers/w35046

17 Erik Brynjolfsson, Avinash Collis, W. Erwin Diewert, Felix Eggers, and Kevin J. Fox, “GDP-B: Accounting for the Value of New and Free Goods,” American Economic Journal: Macroeconomics, October 2025. https://www.aeaweb.org/articles?id=10.1257/mac.20210319

18 METR, “Measuring AI Ability to Complete Long Tasks,” March 19, 2025. https://metr.org/blog/2025-03-19-measuring-ai-ability-to-complete-long-tasks/

19 “State Council issues guideline to implement AI Plus Initiative,” Global Times, August 26, 2025. https://www.globaltimes.cn/page/202508/1341775.shtml

20 “Global AI Governance Action Plan,” Ministry of Foreign Affairs, People’s Republic of China, July 2025. https://www.mfa.gov.cn/eng/xw/zyxw/202507/t20250729_11679232.html

21 “The Political Limits of China’s AI Diffusion Ambitions,” Lawfare. https://www.lawfaremedia.org/article/the-political-limits-of-china-s-ai-diffusion-ambitions

22 “LLM API Pricing Comparison (2025),” IntuitionLabs. https://intuitionlabs.ai/articles/llm-api-pricing-comparison-2025

23 2026 AI Index Report, Stanford Institute for Human-Centered Artificial Intelligence, April 2026. https://hai.stanford.edu/research/ai-index-report

24 Xinhua, “Alibaba’s Qwen tops 700 million Hugging Face downloads,” January 13, 2026.

25 Global Times, “Chinese AI models sweep OpenRouter top six,” April 8, 2026.

26 Erica Chenoweth and Maria J. Stephan, Why Civil Resistance Works: The Strategic Logic of Nonviolent Conflict, Columbia University Press, 2011. https://cup.columbia.edu/book/why-civil-resistance-works/9780231156820

27 Erica Chenoweth, “Questions, Answers, and Some Cautionary Updates Regarding the 3.5% Rule,” Carr Center Discussion Paper, Harvard Kennedy School, 2020.

28 “Defeating Tyranny with the 3.5 Percent Rule,” American Bar Association, October 2025. https://www.americanbar.org/groups/crsj/resources/human-rights/2025-october/defeating-tyranny/

29 Walter Scheidel, The Great Leveler: Violence and the History of Inequality from the Stone Age to the Twenty-First Century, Princeton University Press, 2017. https://press.princeton.edu/books/paperback/9780691271842/the-great-leveler

30 Peter Turchin, End Times: Elites, Counter-Elites, and the Path of Political Disintegration, Penguin, 2023. https://peterturchin.com/book/end-times/

31 Peter Turchin, “Political instability may be a contributor in the coming decade,” Nature 463, 608 (2010). https://www.nature.com/articles/463608a

32 Daron Acemoglu and James A. Robinson, Why Nations Fail: The Origins of Power, Prosperity, and Poverty, Crown Business, 2012.

33 Carles Boix, Democracy and Redistribution, Cambridge University Press, 2003.

34 Alvin W. Graylin, “Abundanism: A New Philosophy for a Post-Scarcity World,” Abundanist Substack, May 13, 2025. https://abundanist.substack.com/p/abundanism

35 Alvin W. Graylin, “Beyond Rivalry: A US-China Policy Framework for the Age of Transformative AI,” The Digitalist Papers, Volume 2, Stanford Digital Economy Lab, December 2025. https://www.digitalistpapers.com/vol2/graylin

36 Alvin W. Graylin, “Misdiagnosing the U.S.-China AI Race: Recalibrating America’s Approach to an Incomplete Strategy,” Center for China Analysis, Asia Society Policy Institute, May 1, 2026. https://centerforchinaanalysis.asiasociety.org/p/misdiagnosing-the-uschina-ai-race

37 “U.S. can hold AI talks with China because ‘we are in the lead,’ Bessent tells CNBC,” CNBC, May 14, 2026. https://www.cnbc.com/2026/05/14/us-china-ai-rules-bessent-us-lead.html

38 Paul Triolo, “A Costly Illusion of Control: No Winners, Many Losers in U.S.-China AI Race,” The Cairo Review of Global Affairs. https://www.thecairoreview.com/essays/a-costly-illusion-of-control/

39 Erik Brynjolfsson et al., “Canaries in the Coal Mine: Six Facts about the Recent Employment Effects of Artificial Intelligence,” Stanford Digital Economy Lab. https://digitaleconomy.stanford.edu/publication/canaries-in-the-coal-mine-six-facts-about-the-recent-employment-effects-of-artificial-intelligence/

40 “Anthropic’s plea for US to grow its AI edge over China is ‘irresponsible’: analysts,” South China Morning Post. https://www.scmp.com/tech/tech-trends/article/3353756/anthropics-plea-us-grow-its-ai-edge-over-china-irresponsible-analysts

41 Elliot Jones, “A ‘CERN for AI’—What Might an International AI Research Organization Address?” Chatham House, June 2024. https://cfg.eu/building-cern-for-ai/

42 Our World in Data Energy Per Capita Chart: https://ourworldindata.org/grapher/per-capita-energy-use?tab=line&country=IND~USA~CHN~FRA~GBR~ZAF~JPN~DEU~BRA

43 Nordhaus, W. D. (2002). Productivity Growth and the New Economy. Brookings Papers on Economic Activity, 2002, 211–265. https://doi.org/10.1353/eca.2003.0006

44 Alvin W. Graylin, Louis Rosenberg, “Our Next Reality” (Hachette, 2024) www.ournextreality.com

The narrated audio version of this essay filled a perfect gap in my afternoon today during a long drive to an appointment in Jupiter, FL This thoughtful call to action should be required for all policymakers, corporate leaders and stakeholders, as well as community leaders and organizers. Thank you Alvin for sharing your insights in such an approachable and accessible way.

Well done Alvin. Super clear narrative, super convincing conclusion. I agree with your take, this over-enthusiastic passion in a new technology is the hallmark of American capitalism, which provides the blood and energy of its society, as well as the economic rollercoaster excitement. Well, I hope this 3.5% isn't sharpening their pitchforks, and those AI titans can come to realization before the village gets burned down.